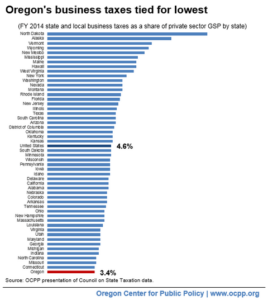

Oregon is tied for the nation’s lowest business taxes in a study conducted by the accounting firm Ernst & Young for the Council On State Taxation (COST). The COST study purports to total all state and local taxes paid by businesses or passed through to business owners and then compares that total to the size of each state’s private sector economy. That results in what COST calls the “total effective business tax rate” for each state. Oregon’s 3.4 percent total effective business tax rate is tied with Connecticut for the lowest in the nation.[1]

A proposed increase in Oregon’s corporate minimum tax for C-corporations with more than $25 million in in-state sales would place Oregon in the middle of the pack in terms of its total effective business tax rate, based on a preliminary revenue estimate for the measure.[2]

COST: Oregon’s State and Local Taxes are Lowest in Nation

The 2015 edition of the COST study – Total State and Local Business Taxes: State-by-State Estimates – which examined data for states’ fiscal years ending in 2014, ranked Oregon as tied for the nation’s lowest total effective business tax rate. Only Connecticut ranked as low as Oregon.

The COST study purports to include all the state and local taxes paid by businesses. These taxes include corporate income and excise taxes; property, sales, and use and license taxes paid by businesses; personal income taxes on business income passed through to the personal income tax (such as those paid by owners of S-corporations and limited liability companies); unemployment insurance taxes; and other business taxes.

COST does not disclose the details of all the taxes included, only a general description that implies that Ernst & Young includes all taxes on all businesses.

State and local taxes paid by businesses amounted to 3.4 percent of Oregon’s private sector gross state product (GSP) in fiscal year 2014. Both the national average and the median were 4.6 percent.

COST Is Not Alone in Saying Oregon Has Nation’s Lowest Business Taxes

Oregon also ranked lowest in terms of total state and local business taxes in a recent study by the Anderson Economic Group (AEG), which looked at data from fiscal year 2013.[3] Instead of comparing taxes collected to GSP as done by COST, AEG examined taxes paid by businesses as a share of “pre-tax operating margin,” one measure of profits. The AEG study considers taxes paid by businesses, such as property, license, personal income on pass through entities, corporate income, unemployment compensation, severance, general sales and gross receipts, and other selective sales taxes. AEG notes that it does not consider the incidence of those taxes; in other words, AEG does not consider whether the business taxes are paid by consumers, shareholders or employees. Comparing the AEG study with an earlier COST report for the same tax year, the studies arrived at different estimates of business taxes paid.

Despite the different methodology employed by AEG, Oregon still came up as having the nation’s lowest business taxes.

What Would “A Better Oregon” Tax Proposal Do to Oregon’s Ranking?

The group A Better Oregon is circulating an initiative petition for the 2016 election that would increase the state’s corporate minimum tax for C-corporations with Oregon sales above $25 million a year. For C-corporations with in-state sales above $25 million, the measure would levy a 2.5 percent tax in addition to the $30,000 minimum tax they pay on the first $25 million in sales. Under this proposal, those C-corporations would pay the greater of this new minimum tax or the existing tax on corporate profits.

Based on a preliminary projection of what the tax would raise each year, such a change would place Oregon in the middle of the pack (25th) in terms of the total effective business tax rate.[4] The Legislative Revenue Office preliminarily estimated that the measure would raise an additional $5.3 billion in the 2017-19 budget period.[5] Assuming one year of that revenue ($2.65 billion) were added to Oregon’s collections in 2014, Oregon’s total effective business tax rate would have been 4.7 percent. Both the national average and the median were 4.6 percent in 2014.

Public Investments, Not Low Taxes, Create a Strong Business Climate

Tax rates matter relatively little when it comes to where companies choose to locate. State and local taxes constitute a small share of the cost of doing business — less than 2 ½ percent of total expenses.[6] A survey of entrepreneurs found that they rarely cited taxes as a factor for choosing a particular location for their business.[7] Instead, their top concerns were quality of life, the presence of a talented pool of workers and access to customers and suppliers.[8]

Quality public schools and universities, a good transportation system and public amenities such as parks and libraries are the kinds of public structures that attract employers and foster a good business climate. Strong public schools, in particular, are critical to recruiting and retaining a skilled labor force. Families consider the quality of school systems when deciding where to live and work.

The COST study itself acknowledges that state spending, supported in part by business taxes, benefits businesses. For example, it recognizes that education funding — the largest category of state and local spending — can help improve profits and businesses’ return to capital.[9]

In summary, Oregon can strengthen its business climate by creating a top-notch education system and upgrading our public infrastructure. That strategy requires tax revenue to make it happen. The COST study indicates that businesses can pay more.

[1] COST represents more than 600 multistate corporations. While COST does not disclose its current list of members, as recently as 2010 Nike and Intel belonged to the council. The study does not provide a detailed methodology to confirm the findings. To read the report see Total state and local business taxes: State-by-state estimates for fiscal year 2014, Council on State Taxation, October 2015

[2] Initiative Petition 28 for 2016 General Election, A Better Oregon, February 2015.

[3] 2015 State Business Tax Burden Rankings, Anderson Economic Group, June 2015.

[4] OCPP analysis of Bureau of Economic Analysis and Council On State Taxation data.

[5] Revenue estimates for Initiative Petition 28 prepared by Legislative Revenue Office, July 13, 2015.

[6]OCPP analysis of Internal Revenue Service (IRS) Statistics of Income (SOI) and Council On State Taxation data.

According to IRS SOI data, corporations nationwide deducted $546.1 billion in federal, state and local taxes in fiscal year 2012, making up about 2.0 percent of the total expense deductions of $27.7 trillion for corporations that year.

In fiscal year 2012, COST estimated that state and local taxes paid by businesses – not just corporations – totaled $624.4 billion (see Total state and local business taxes: State-by-state estimates for fiscal year 2012, Council On State Taxation, July 2013). If you assume that all these taxes were paid by corporations (they were not), they would have amounted to just 2.3 percent of all corporate expenses (of $27.7 trillion).

For more on methodology and COST’s claims about IRS data, see end note 5 in Mazerov, Michael, Vast Majority of Large New Mexico Corporations Are Already Subject to “Combined Reporting” in Other States, Center on Budget and Policy Priorities, January 26, 2010, p. 6, available at http://www.cbpp.org//sites/default/files/atoms/files/1-26-10sfp.pdf.

[7] What do the Best Entrepreneurs Want in a City? Lessons from the Founders of America’s Fastest Growing Companies, Endeavor Insight, February 6, 2014.

[8] Ibid. See also The State of Main Street: Oregon small business views on state and national public policy, Main Street Alliance, October 2014.

[9] Total state and local business taxes: State-by-state estimates for fiscal year 2014, Council on State Taxation, October 2015, pp. 16-17.

The COST study publishes a ratio purportedly showing how many dollars a business is taxed for every dollar it receives in benefits from government spending. The higher a state ranks, the lower its ratio. While this “vending-machine” view of the tax system is misguided, the COST study acknowledges that businesses benefit from the government spending that taxes make possible.

The study calculates the ratio in three ways depending on the extent to which education spending is assumed to benefit businesses. The study estimates this ratio assuming that no education spending benefits businesses, that 25 percent of education spending benefits businesses, and that 50 percent of education spending benefits businesses.

Regardless of which assumption is considered, Oregon ranked in the bottom half of states in terms of business taxes per dollar of state and local government expenditures benefiting businesses in 2014. It ranked 31st (tied with 11 other states) when assuming 50 percent of education spending benefits businesses.

In 2009, COST’s report pegged Oregon as tied for the lowest — most favorable to businesses — ratio when assuming half of education spending benefits businesses.

What caused Oregon’s drop in rankings is not clear. Beyond the assumptions as to what extent education spending benefits businesses, it is unclear what the COST study considers in its analysis. And even if this analysis is valid, what is clear is that Oregon’s drop in the rankings is not due to taxes increasing, as Oregon had the lowest total effective business tax rate in 2009 and 2014.