This report is also available as a PDF: Workers versus owners: a fault line of inequality

It’s not just the amount of income that separates the richest from ordinary Oregonians; it’s also the type of income. Understanding the differences helps identify policies that reduce inequality, rather than exacerbate it.

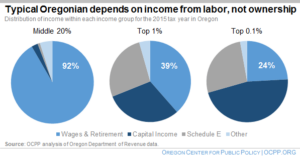

Ordinary Oregonians make a living mostly from a paycheck — wages earned from work.[1] If you divide all Oregonians into five groups by income, the group in the middle earned between $29,000 and $51,000 in 2015.[2] For this middle-income group, wages and retirement income made up about 92 percent of all income.[3] Wages alone made up 77 percent.

By contrast, a large share of the income of the richest Oregonians comes from their ownership of assets and businesses. The average member of the top 1 percent made over $1 million in 2015. About 39 percent of that amount came from wages and retirement income. Another 30 percent came from their ownership of capital — capital gains income, dividends, and interest income (“capital income”). Still another 27 percent of the top 1 percent’s income was reported on federal tax form Schedule E. Schedule E includes income from rental properties, royalties, partnerships, S corporations, estates, trusts, and residual interests in real estate mortgage investment conduits.[4]

The ownership of assets and businesses makes up an even bigger source of income for the richest 1 out of 1,000 Oregonians, the top one-tenth of 1 percent. For this group, who have an average income of about $4.3 million, capital income added up to 46 percent of their income in 2015. Schedule E income accounted for another 27 percent. Income from wages and retirement made up only 24 percent of their income.

Addressing income inequality, arguably the “defining challenge of our time,” requires an understanding of the types of income accruing to Oregonians at different rungs of the economic ladder.[5] Simply put, confronting inequality requires policies that bolster wages. It also requires taxing income from capital or from ownership of businesses the same as income from wages, rather than giving that income special treatment.[6]

[1] The term Oregonians is used as a short-hand for Oregon tax filers throughout this publication. Often the unit filing taxes includes more than one Oregonian, as in a married couple filing jointly.

[2] Income in this publication is the total income reported on IRS tax forms. This does not include adjustments, deductions, subtractions, credits or any other modifications to reported income.

[3] All data include all full-year resident tax returns for the 2015 tax year.

[4] The income not included in this discussion is labeled in the chart as “other”. This includes income that is called “other” and “business income” in the Oregon Department of Revenue data provided to OCPP.

[5] President Barack Obama, “Remarks by the President on Economic Mobility,” December 4, 2013.

[6] In 2013, the Oregon legislature created a special tax rate for certain types of Schedule E income. In 2017, the Oregon House passed a bill that would have reduced this “suits and scrubs” tax break, but the Oregon Senate chose not to consider it. Read more at OCPP, June 2017.