Rural counties stand at a disadvantage when it comes to the benefits doled out by Oregon’s largest housing subsidy, the mortgage interest deduction. Taxpayers in a

few urban counties capture a disproportionate share of the housing subsidy, projected to cost Oregon over $1 billion in the upcoming budget period. That is not surprising, given that the mortgage interest deduction mainly benefits well-off taxpayers, who tend to be concentrated in urban areas.

This paper examines Internal Revenue Service data on taxpayers’ use of the federal mortgage interest deduction in tax year 2014. Because the Oregon mortgage interest deduction is based on the federal deduction, the distribution of the Oregon deduction is likely to be similar to the federal deduction.

The mortgage interest deduction is a subsidy for some homeowners. It allows those who can claim it to reduce their taxable income by the amount of interest paid on their mortgage.[1] The savings to the taxpayer is the deductible amount multiplied by their top tax bracket.[2]

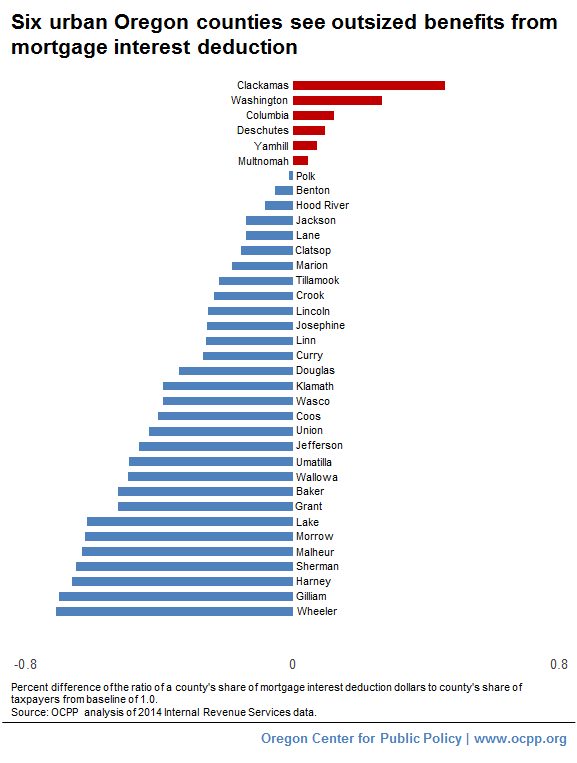

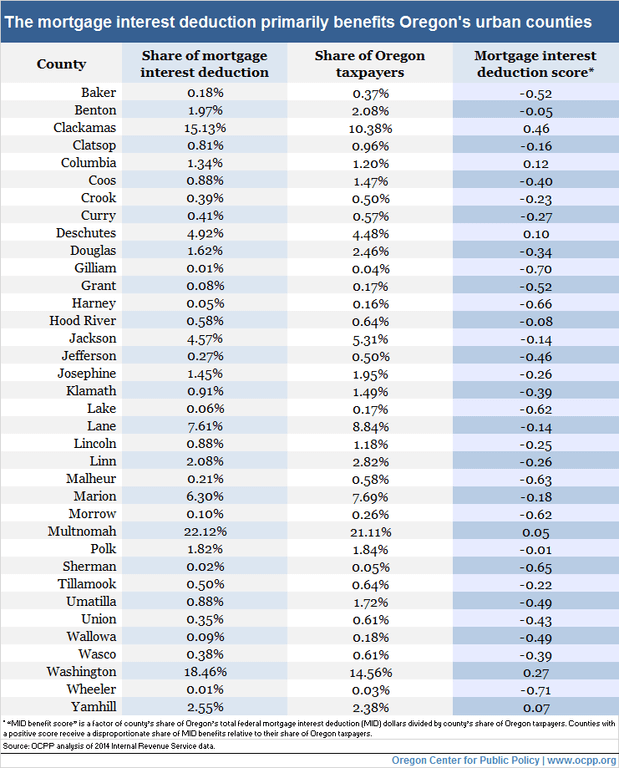

Taxpayers in six urban counties received a disproportionate share of the deduction’s value in 2014.[3] Clackamas, Washington, Columbia, Deschutes, Yamhill and Multnomah Counties each saw a greater share of mortgage interest deduction dollars than the county’s share of Oregon taxpayers. Taxpayers in all other counties received a smaller share of mortgage interest deduction benefits than their share of taxpayers. (See the fact sheets for each Oregon county below.)

In 2014, taxpayers in Oregon’s urban counties took nearly 87 percent of the tax savings from the federal mortgage interest deduction. More than half (55.7 percent) of the benefits went to taxpayers in Clackamas, Multnomah, and Washington Counties, the three counties in the Portland metro area.

That taxpayers in urban counties take the lion’s share of mortgage interest deduction dollars is not surprising, given that the deduction mainly benefits those better off financially, who tend to be concentrated in urban areas. There are several reasons why the deduction steers most of the benefits to those on the upper end of the income scale. First, the mortgage interest deduction only helps homeowners, and higher-income earners are more likely to own a home than lower-income earners. Second, the subsidy only helps those who itemize deductions and they are disproportionately higher-income earners. And third, because it is a deduction from taxable income (not a credit against taxes), every dollar deducted reaps more valuable tax savings to those with more income in the top tax brackets — the wealthy.[4]

Confront Oregon’s housing crisis by reforming the mortgage interest deduction

Oregon is in the midst of a statewide housing crisis, with many families struggling to keep a roof over their heads. Oregon’s mortgage interest deduction — the state’s largest housing subsidy at $1.1 billion a budget period — does little, if anything, to address that crisis.[5] Instead, the mortgage interest deduction mainly helps those who do not need help buying a home, exacerbating economic inequality, which is at historic levels.[6] This analysis shows it also deepens the urban-rural economic divide.

State lawmakers should reform the billion-dollar mortgage interest deduction so that it becomes an effective tool for addressing Oregon’s housing affordability crisis. Lawmakers can reform the deduction in a way that preserves the benefits for low and middle-income homeowners, while phasing out the benefits for higher income homeowners who do not need a tax subsidy to afford their home. Doing so would free up substantial resources for the state to put toward homeownership and other housing opportunities for families struggling with skyrocketing housing costs.

County fact sheets

Benton

Clackamas

Clatsop

Columbia

Coos

Crook

Curry

Deschutes

Douglas

Gilliam

Grant

Harney

Hood River

Jackson

Jefferson

Josephine

Klamath

Lake

Lane

Lincoln

Linn

Malheur

Marion

Morrow

Multnomah

Polk

Sherman

Tillamook

Umatilla

Union

Wallowa

Wasco

Washington

Wheeler

Yamhill

[1] Taxpayer who can claim the deduction can deduct interest paid mortgage debt up to $1 million, be it from a first or second home (or both), and interest paid on home equity debut up to $100,000.

[2] In Oregon, the tax brackets are 7, 9, and 9.9 percent.

[3] Unless otherwise noted, all figures in this report are OCPP analysis of Internal Revenue Service data.

[4] The Mortgage Interest Deduction: Oregon’s Biggest (and Ineffective) Housing Subsidy, Oregon Center for Public Policy, May 4, 2015.

[5] Research shows that the mortgage interest deduction is ineffective when it comes to meeting its stated purpose of promoting homeownership, likely because the deduction is capitalized into home prices. For more see Steven C. Bourassa, Donald R. Haurin, Patric H. Hendershott, and Martin Hoesli, “Mortgage Interest Deductions and Homeownership: An International Survey,” Swiss Finance Institute Research Paper No. 12-06, March 13, 2013. Additional research suggests that where the deduction may have a positive effect on homeownership, it only does so for, “higher income households in less tightly regulated housing markets.” For more see Christian A. L. Hiber and Tracy M. Turner, “The Mortgage Interest Deduction and its Impact on Homeownership Decisions,” Spatial Economics Research Centre, Discussion Paper 55, September 2010.

[6] The Congressional Budget Office estimates that the benefits of the mortgage interest deduction equal, “less than 0.1 percent of after-tax income for households in the lowest income quintile, 0.3 percent for those in the middle quintile, and 1.1 percent for those in the highest quintile.” For more see The Distribution of Major Tax Expenditures in the Individual Income Tax System, Congressional Budget Office, May 2013.

Related materials:

News release: Rural Oregonians get meager share of Oregon’s biggest housing subsidy , February 21, 2017

Blog post: Who needs a housing subsidy more?, March 31, 2017

Blog post: A ready-made solution for protecting Oregon’s homeless children, March 24, 2017

Blog post: The rich families’ down-payment assistance program, March 10, 2017