Creating a personal income tax credit to address the impact of a proposed commercial activities tax (CAT), instead of reducing personal income tax rates, would strengthen a tax reform plan currently under discussion in the Oregon legislature. This new tax credit (the “CAT Fairness Credit”) would target relief to low- and middle-income groups — taxpayers with income below $64,000 — while raising more revenue to invest in schools and essential services.

Oregon lawmakers should be applauded for exploring tax reform that would raise significant revenue from businesses to fund services that benefit all Oregonians. The state needs an additional $1.4 billion in revenue in the upcoming budget period just to keep services at their current level. On top of that, Oregon needs to invest an additional $2 billion in the upcoming budget period to meet the state’s quality education goals.[1] It needs even more to establish a universal preschool system, make college affordable for all families, ensure all Oregonians have access to quality health care, adequately protect abused and neglected children, and address the statewide housing crisis.

Download a copy of this fact sheet

Commercial Activities Tax Fairness Credit Would Strengthen the Tax Reform Package (PDF)

The tax reform concepts being discussed by the Joint Committee on Tax Reform contain three elements: enacting a commercial activities tax (CAT), repealing the corporate income tax (CIT), and lowering personal income taxes as a corrective measure to offset increased costs to consumers associated with the change in the way businesses are taxed.

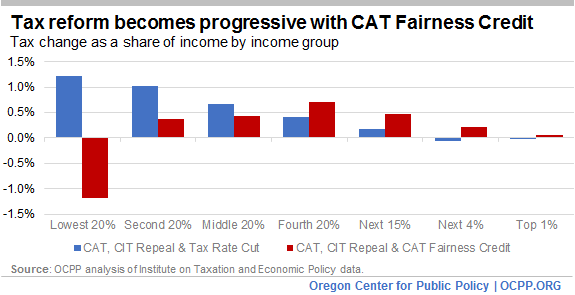

The legislature can improve the overall tax package by replacing the personal income tax rate reduction scheme with a CAT Fairness Credit. The CAT Fairness Credit would cost less than the income tax rate reductions and better target relief to low- and middle-income taxpayers, strengthening the overall package.

CAT Fairness Credit: A targeted and less costly option

By making one change to the tax reform package currently under discussion, the legislature can significantly strengthen the package. That change is replacing the proposed personal income tax rate reduction scheme with a CAT Fairness Credit. A CAT Fairness Credit would cost 13 percent less than the proposed change in personal income tax rates. Thus, a CAT Fairness Credit would yield more revenue, furthering a main goal of tax reform. This approach would also better target tax relief to low- and middle-income households and avoid exacerbating income inequality.

Analysis by the Institute on Taxation and Economic Policy (ITEP) shows that, all else being equal, a tax reform package with a CAT Fairness Credit would be more progressive than a tax reform package with an income tax rate reduction.

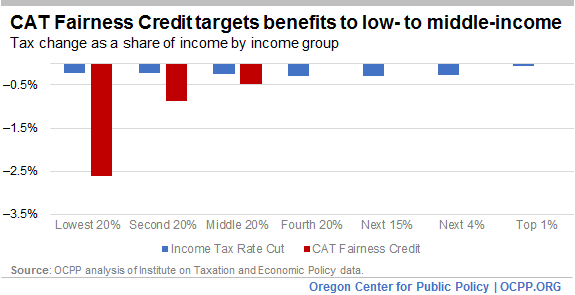

While cuts in income tax rates affect taxpayers across the income spectrum, a CAT Fairness Credit is targeted to low- and middle-income households. Such a credit would be larger for lower income taxpayers, for those with larger families, and for elderly Oregonians. The CAT Fairness Credit would be refundable, so taxpayers would get the full credit to offset the costs of the CAT even if it exceeded their personal income tax liability.[2] (See Appendix for details of CAT Fairness Credit.)

By design, the CAT Fairness Credit would provide a tax cut only for taxpayers in the bottom three quintiles — low- to middle-income Oregonians. The credit is progressive, as the tax change as a share of income is greater the lower the household income.

As recognized by proponents of the tax package, a commercial activities tax needs a corrective measure due to impact on consumers

A commercial activities tax is a tax applied to a business’s gross receipts in Oregon. Oregon’s current corporate minimum tax is a gross receipts tax. The amount of revenue a CAT raises depends on which receipts it covers (the “base”) and the rate or rates applied to those receipts.

A gross receipts tax differs from a sales tax in that only part of the tax is passed on to consumers and some of it is exported out of state.[3] While economists differ on what percent is passed on to in-state consumers, they are generally in agreement that the amount passed on from a CAT is greater than the amount passed on by a corporate income tax on profits. That is why proponents of the tax reform package include changes to the personal income tax in addition to changing how Oregon taxes businesses. The CAT also falls more heavily on lower income taxpayers than a corporate income tax.[4]

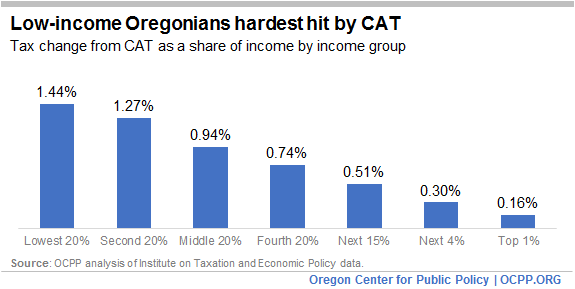

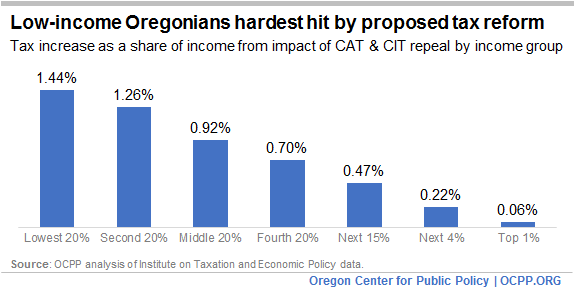

To the extent the tax is passed on to Oregon consumers, a CAT impacts low- and middle-income households the hardest. ITEP estimates the impact of an Oregon CAT on low- to middle-income taxpayers would be as much as nine times greater, as a share of income, than the impact on the top 1 percent of households.

Low- and middle-income working Oregonians already struggle with child care costs, housing affordability, and food insecurity.[5] Thus, a well-designed protection against the impacts of the tax on these vulnerable Oregonians should accompany a commercial activities tax.

Note on CAT design used in this analysis

The Joint Committee on Tax Reform has seen several tax reform options, all of which feature a CAT. Every proposal has included a CAT coupled with the repeal of the corporate income tax and reductions to three of Oregon’s four personal income tax rates. The proposals have varied the CAT tax rate(s) and thresholds. This analysis is based on a rate in the range of the various rates considered to date — 0.8 percent — and a threshold of $1 million. The comparison with personal income tax rate reductions in this paper uses the half percentage point reductions to the first three brackets used in many of the proposals under consideration.[6] Once the CAT design is finalized (rates and threshold), the CAT Fairness Credit should be adjusted to address the impacts of the final version.

Repeal of the corporate income tax has regressive effects, adding to the need for a targeted, corrective personal income tax provision

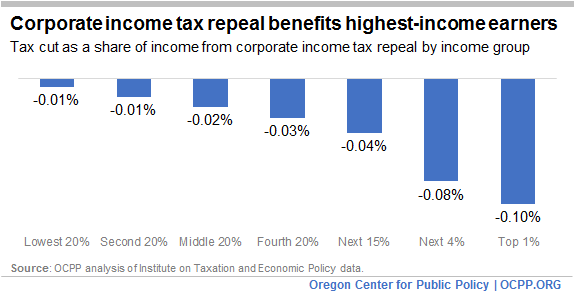

The tax reform proposals under discussion would pair the enactment of a CAT with the repeal of the corporate income tax. Analysis by ITEP concludes that the tax reduction as a share of income from repeal of the corporate income tax would be greater for those at the top of the income scale than for those at the bottom. The tax change experienced by the top 1 percent would be about 10 times the change experienced by the lowest income group.

Thus, repealing the corporate income tax would exacerbate the distributional problem caused by CAT costs being passed on to consumers. As noted in the chart below, when looked at together, the impact as a share of income on the lowest income group (1.44 percent) is 24 times the impact on the top 1 percent (0.06 percent).

Cutting income tax rates to correct the problem is costly and poorly targeted

All of the proposals thus far considered by the Joint Tax Reform Committee recommend offsetting some of the costs to consumers by reducing the tax rates in the first three of Oregon’s four personal income tax brackets. Oregon taxes some income at 5 percent, a little more income at 7 percent, and still more income at 9 percent. Once someone’s income reaches the top bracket ($250,000 for couples), all of the income over that level is taxed at 9.9 percent.

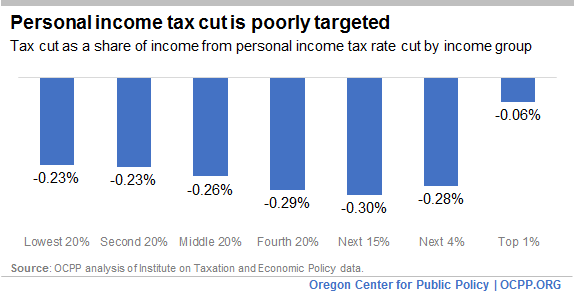

Proposals to offset the impact of the CAT on consumers by reducing personal income tax rates are poorly targeted and unnecessarily costly. Every taxpayer gets to use each of the lower personal income tax brackets, making that type of rate reduction a tax cut for everyone, even those at the top of the income ladder who are already reaping a disproportionate share of our growing economy.[7] As shown above, the tax cut as a share of income generally increases as you go up the income ladder under a rate reduction scheme.

Reducing the rates is expensive in comparison to the CAT Fairness Credit. According to the Legislative Revenue Office (LRO), reducing the three lower tax rates to 4.5, 6.5 and 8.5 percent would cost about $548 million in foregone revenue in the 2017-19 budget period, $837 million in 2019-21, and $914 million in 2021-23.[8] The CAT Fairness Credit would cost 13 percent less, according to an analysis by ITEP.

In short, the proposals to reduce personal income tax rates are not targeted to low- and middle-income families and are more costly than a credit.[9]

Other options under consideration are not as well targeted as the CAT Fairness Credit

In their discussions with the Joint Committee, the LRO has proffered options other than the personal income rate reduction scheme for offsetting the costs to consumers of the CAT. None are as targeted as the CAT Fairness Credit. The other options include:

Increasing the personal exemption credit. While the personal exemption credit does take into account family size, it is also available for couples (joint filers) making up to $200,000 per year in income. As such, increasing the personal exemption would not be very well targeted to low- and middle-income households.

Increasing the standard deduction. The standard deduction does not take into account family size. Also, while the well-off are more likely to itemize their tax deductions, some of the wealthiest Oregonians take the standard deduction.[10]Thus, increasing the standard deduction is not very well targeted to low- to middle-income households.

Expanding Oregon’s Earned Income Tax Credit. The Oregon Earned Income Tax Credit (EITC) is an effective program that supports low-wage working families. The Oregon EITC rightly takes into account family size and the age of children. That said, the Oregon EITC provides almost no benefit to individuals without children, and is of no benefit to those who are not able to work because of a disability, or those unable to find work. Low-income elderly Oregonians are unlikely to qualify for the EITC. A CAT Fairness Credit, by contrast, would reach these Oregonians struggling to get by.

Conclusion

The Joint Committee on Tax Reform can improve the tax reform package under consideration by replacing the personal income tax rates reduction scheme with a CAT Fairness Credit. Doing so would maximize resources raised by the tax plan and avoid unnecessarily benefiting high income households who have been disproportionately reaping benefits from economic growth. Raising more revenue to invest in Oregon schools and essential services in the fairest manner is an important goal that can be achieved by incorporating a CAT Fairness Credit instead of personal income tax rate reductions and other options under consideration.

Appendix

The CAT Fairness Credit is designed to be worth a set amount per member of the family based on the income level of the tax filer. Low-income taxpayers would be able to obtain the full benefits of the CAT Fairness Credit because it would be refundable. Like a number of provisions in the personal income tax code, the credit would be indexed to inflation.

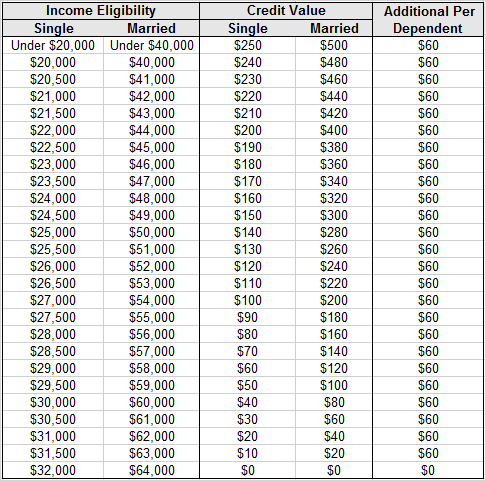

The CAT Fairness Credit would start at $500 for a married couple filing jointly making under $40,000 and $250 for a single filer making less than $20,000. The credit would gradually scale down until reaching a cap of $64,000 for a married couple and $32,000 for a single filer. For each additional child, the credit would provide a $60 tax benefit for filers earning under the maximum. For example, a single filer making $18,000 would receive a $250 refundable tax credit, which would increase by $60 for each child. A married couple filing jointly making $54,500 would receive a $200 credit.

Low-income elderly Oregonians would receive double the tax credit indicated below.

Note: Married includes Head of Household filers. Single includes Married Filing Separately filers.

[1] Quality Education Commission, Quality Education Model Final Report, 2016, p. 11.

[2] It would be a refundable tax credit, not a carried-forward credit, to enable the lowest income taxpayers to fully utilize it.

[3] See Northwest Economic Research Center, The Economic Impacts of a Gross Receipts Tax for Oregon with Implications for Initiative Petition 28, 2016.

[4] Research indicates owners of capital and labor bear the burden of increases to the corporate income tax far more than consumers. See Cronin et al. Distributing the Corporate Income Tax: Revised U.S. Treasury Methodology, 2013, National Tax Journal 66 (1): 239-62.

[5] OCPP, Oregon’s Spike in Food Insecurity Worst Among All States, November 2016.

[6] Proposals found in materials for numerous meetings of the Joint Committee on Tax Reform.

[7] OCPP, Outsized Gains at the Top Worsen Oregon Income Inequality, June 2016.

[8] Simulation results presented to the Joint Committee on Tax Reform by the Oregon Legislative Revenue Office on May 10, 2017.

[9] One way to reduce the amount of the tax cut benefit going to the highest income households is to disallow use of the lower rate brackets for households with high income.

[10] OCPP analysis of Oregon Department of Revenue 2014 tax statistics. 12 percent of the top 20 percent of taxpayers do not use itemized deductions.