It creates favoritism, it’s ineffective, it’s unnecessary and it’s irresponsible

It’s unfortunate that some Oregon lawmakers are pushing to cut the tax rate on income from capital gains. Several legislative proposals exist to grant preferential treatment to income generated from the sale of assets such as stocks, bonds and real estate.

This misguided policy fails on four fundamental levels: it favors some taxpayers over others, it’s ineffective, it’s unnecessary and it’s irresponsible.

Download the full report:

Download just the executive summary (PDF)

Related materials:

Oregon More Than Doubles Its Venture Capital, May 4, 2011

Trade the Kicker for a Boot That Stomps on the Middle Class? No Thanks, April 2011

A Tax Cut That Bleeds Revenue and Penalizes Work, December 2010

Cutting the income tax on capital gains favors speculators over workers and favors the rich over the rest. It would create a situation where ordinary Oregonians working for paychecks would end up paying a higher tax rate on their income than someone who lives off of investment income. For example, the average salary for a teacher in Oregon in 2010 was about $51,000. An educator earning this amount in 2012 would pay a top rate of 9 percent in income taxes. If that year the tax rate on capital gains income were cut in half, someone who is fortunate enough to live off of investment or trust fund income — be it the same amount as the teacher earns or many times that amount — would pay a top rate of no more than 4.95 percent.

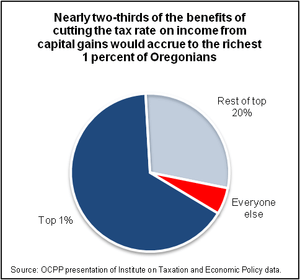

It would also, by and large, constitute a tax cut just for the rich. If Oregon halved the income tax rate on capital gains, the richest 1 percent of Oregonians would get 65 percent of the tax cut. The rest of Oregonians would receive little or nothing.

Cutting the income tax on capital gains is also ineffective as a means to attract investment, contrary to what proponents claim. Research shows that there is no correlation between growth in the economy — real GDP growth — and the tax rate on income from capital gains. Demand for products and services, not the amount of after tax income, is what drives investment. Thus, a general tax cut on income from capital gains will have no real impact on investment. Plus, there’s no guarantee that the money would be reinvested in Oregon. And for those who argue for a targeted tax cut for money reinvested in the state, Oregon’s own experience demonstrates the futility of such an effort.

Cutting the income tax on capital gains is also unnecessary, since Oregon’s economy already tends to outperform the nation as a whole. In recent years, Oregon’s economy has grown faster than that of the nation and has attracted more than its share of venture capital, even though, like a majority of states with income taxes, it taxes income from capital gains the same as any other income. Indeed, more taxpayers with capital gains income move to Oregon than move out, and collectively, in the year of their moves, those arriving have more capital gains than those who leave Oregon.

Finally, cutting the income tax on capital gains is irresponsible. During difficult economic times, income from capital gains constitutes an important source of revenue to fund popular and vital public services. During good economic times the income tax on capital gains shines, often generating more revenue than anticipated. If this unanticipated revenue were saved in the Rainy Day Fund, Oregon would be better positioned to weather bad economic times. By giving preferential tax treatment to income from capital gains, the income tax would not shine so brightly in good years, harming Oregon’s ability both to fund vital and popular public services and to save for rainy days.