Oregon should establish a Wealth Proceeds Tax, a tax focused on the income the wealthy derive from owning assets. At a time when the federal government has curtailed its historical commitment to funding health and nutrition, Oregon will need to step up to address the basic needs of its people. Given the extreme and growing concentration of wealth in the hands of the few, a Wealth Proceeds Tax is a smart way for Oregon to raise the revenue it will need in the coming years.

This paper explains the basics of a Wealth Proceeds Tax and why it makes sense for Oregon to establish this revenue-raising mechanism.

What is a Wealth Proceeds Tax?

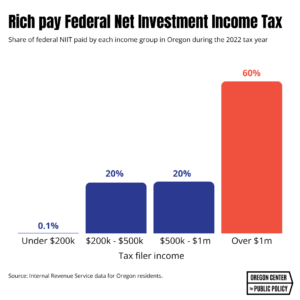

A Wealth Proceeds Tax is designed to tax the money people make from owning things — the income generated from wealth. It piggybacks on an existing federal tax called the Net Investment Income Tax (NIIT), established in 2010 to fund the Affordable Care Act. The NIIT applies a 3.8 percent tax on certain income over $200,000 for single individuals and $250,000 for joint filers earned from owning assets. Currently, only 4 percent of Oregonians pay the federal NIIT. Of that group, more than 60 percent of Oregonians paying the NIIT make more than $1 million per year.

What type of income derived from owning assets could be subject to the Wealth Proceeds Tax?

A Wealth Proceeds Tax based on the NIIT would generally apply to passive income derived from owning assets, not income from work. Specifically, it applies to:

- Interest

- Dividends

- Capital gains

- Rental and royalty income

- Nonqualified annuities

- Passive income from a pass-through entity

It does not apply to many other forms of income, such as:

- Sole proprietor income[1]

- Income from selling an actively managed pass-through business (LLC, partnership, etc.)

- Income from tax-advantaged retirement accounts (Social Security, 401(k), pensions, and IRAs)

- Up to $500,000 in income from the sale of a primary residence, and more

Why does Oregon need a Wealth Proceeds Tax?

While there are various reasons Oregon should have a Wealth Proceeds Tax, two are the most important. First, wealth and income inequality are corroding our collective economic vitality and social well-being, and tax policy is making it worse. The Wealth Proceeds Tax would be a direct response to this growing inequality by targeting taxes on the very things that make the rich richer. Second, Oregon’s budget has been thrown into disarray by federal actions. Raising revenue quickly and efficiently from those most able to pay is an urgent necessity.

How does the Wealth Proceeds Tax address inequality?

Over the past several decades, the concentration of wealth in the hands of a relative few has reached stratospheric levels. Presently, the wealthiest 1 percent of Oregonians together own more than the bottom 90 percent of Oregonians. Worse still, the combined wealth held by Oregon’s three billionaires is more than twice the wealth of the bottom half of all Oregonians combined.

Part of the reason why wealth inequality has reached extreme levels is that the federal government taxes some forms of income from wealth — such as capital gains from selling stocks and fees for managing hedge funds — at much lower levels than income from a paycheck. Although Oregon generally does not provide preferential tax treatment to income from wealth, a state Wealth Proceeds Tax can serve as a corrective to federal tax policy that weighs more heavily on workers than on the wealthy.[2]

Why is now a good time for Oregon to enact a Wealth Proceeds Tax?

Oregon’s budget will be under severe strain in the coming years because the state will need to backfill cuts to the nation’s safety net enacted by Congress. In 2025, the Republican majority in Congress passed H.R.1. This budget package slashed funding for health care, nutrition assistance, and other essential services to offset some of the costs of massive tax cuts mainly benefiting the rich and corporations.

Because of this, Oregon will need to spend billions to prevent more families from going hungry or without health coverage. In the upcoming budget period (2027 – 2029), the Oregon Health Authority estimates needing more than $4 billion to maintain the Oregon Health Plan, and the Oregon Department of Human Services estimates needing more than $1 billion to maintain the Supplemental Nutrition Assistance Program (SNAP). To prevent this from happening, the legislature will need to find new sources of revenue.

Who would pay the Wealth Proceeds Tax?

A Wealth Proceeds Tax modeled on the NIIT ensures that it only applies to the wealthy through a combination of two mechanisms. First, there is a means test. The tax only applies to single filers with yearly income above $200,000 ($250,000 for joint filers). Second, it only applies to forms of income derived from owning assets — assets mainly owned by the wealthy. Currently, only 4 percent of Oregonians pay the federal NIIT. Of that group, more than 60 percent of Oregonians paying the NIIT make more than $1 million per year. That means around 96 percent of Oregonians would not be touched by a Wealth Proceeds Tax. Only the rich would be subject to it, and the majority paying it would be the extremely rich.

Do any states have a Wealth Proceeds Tax?

Yes. Minnesota created a Wealth Proceeds Tax in 2023 that is similar to the NIIT but starts at $1 million of income. Its low 1 percent rate and higher threshold is still expected to raise more than $60 million next year. New proposals are bubbling up across the country to seize this opportunity, including in Hawaii, Rhode Island, Vermont, and Virginia.

Would the Wealth Proceeds Tax be difficult to administer?

No. An Oregon Wealth Proceeds Tax would simply piggyback on the existing NIIT, which is fairly simple. In fact, the federal tax form for filing NIIT is only one page. If it were to exactly mirror the federal tax break in terms of the types of income it would apply to, then the Oregon Wealth Proceeds Tax would simply be a percentage of the federal amount. From the perspective of the tax filer, complying with an Oregon Wealth Proceeds tax would not be administratively difficult, given that they already provide the relevant information to the IRS.

Are there ways for Oregon to improve on the federal NIIT?

Yes. Oregon can improve on the federal NIIT by expanding it to some forms of income from wealth not included in the federal tax and making other technical improvements related to its tax code:

- While a robust starting point, the federal NIIT exempts certain long-term capital gains and interest on out-of-state bonds. Ensuring that all gains included in the federal individual income tax are included in the Wealth Proceeds Tax base would improve fairness and stability, and increase revenue.

- The NIIT leaves out income from Qualified Small Business Stock (QSBS). QSBS is a federal tax break on capital gains income for investors — overwhelmingly very wealthy investors — in start-up companies. Until recently, Oregon mirrored the federal tax code by replicating QSBS until the Oregon legislature “disconnected” from QSBS in 2026. If Oregon were to enact a Wealth Proceeds Tax, it would make sense that the new tax would apply to these capital gains.

- Since Oregon would be starting from a federal definition of NIIT, the connection date should also be a point-in-time date (static) rather than a rolling (automatic) connection.

- Oregon should ensure that certain trusts exploited to avoid taxation are no longer an off-ramp in Oregon by linking the income of incomplete non-grantor trusts to the person who created the trust.

- To avoid significant disparities between active and passive pass-through business income, Oregon should eliminate the reduced tax rates for active pass-through business income under the Wealth Proceeds Tax thresholds of $200,000 (single) and $250,000 (joint).

How much revenue would an Oregon Wealth Proceeds Tax raise?

How much an Oregon Wealth Proceeds Tax would raise depends on what types of income it would apply to. If it simply replicated the federal NIIT, each 1 percentage point of an Oregon Wealth Proceeds Tax would generate an estimated $96 million per year, or about $192 million per budget period. An enhanced Wealth Proceeds Tax that includes all long-term capital gains and interest on out-of-state bonds (recommendation #1 above) would raise an estimated $120 million per year, or $240 million per budget period. Following recommendations 2-5 would raise increasingly more revenue from wealthy investors and owners.

Are there other advantages to instituting a Wealth Proceeds Tax?

Given that income from wealth is largely a function of the tax filer’s wealth, the Wealth Proceeds Tax is likely to tax an imperfect, but similar, reflection of the wealth distribution. Due to historic policy choices and structural social inequities, the wealth and assets are heavily concentrated in the hands of white Non-Hispanic people nationwide and here in Oregon. According to the Institute on Taxation and Economic Policy, “Eighty two percent of stock held by people with incomes high enough to be subject to the NIIT is held by white families, even though white families make up just 67 percent of households overall.”

Conclusion

An Oregon Wealth Proceeds Tax is an idea whose time has come. It would help Oregon address a looming fiscal crisis caused by the massive budget package enacted by Congress last year that slashed nutrition assistance and health care to pay for tax cuts for the rich and corporations. And it would help push back against rising economic inequality. That is a win for Oregonians.

[1] Federally, sole proprietor income is excluded because the Health Insurance and Additional Medicare Tax already apply to that income.

[2] Oregon provides preferential tax treatment to one type of income: the profits received by active owners of eligible pass-through businesses and sole proprietorships.