Read this report as a PDF: Schedule E Income Drives Inequality

One of the forces that has propelled income inequality in Oregon to record levels is the concentration of business income and income-producing assets in the hands of the well-off.[1] This can be seen in who reports income on the tax form Schedule E.

Schedule E includes income from rental properties, royalties, partnerships, S corporations, estates, trusts, and residual interests in real estate mortgage investment conduits. Oregonians who only earn income from wages do not file Schedule E. The vast majority of Oregonians (87 percent) do not report any income on Schedule E.

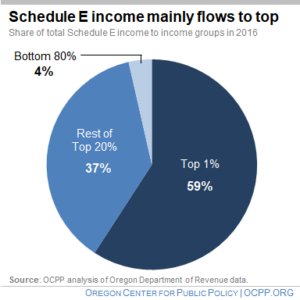

Of all income Oregonians reported on Schedule E in 2016, 59 percent went to the richest 1 percent.[2] The rest of the top 20 percent of Oregonians collected 37 percent. Oregon’s lowest earning 80 percent of taxpayers received only 4 percent of all Schedule E income.

In Oregon, one type of income reported on Schedule E gets special tax treatment. Profits made by partnerships, LLCs and S-corporations are not taxed at the business level, but are “passed through” to the owners, who report those profits as income on Schedule E. Due to a tax break created by the Oregon legislature in 2013, some business owners pay a lower tax rate on their pass-through profits than they would under the ordinary income tax rates.[3] This special tax treatment of one type of Schedule E income exacerbates income inequality, given that Schedule E income mainly flows to the top.

The income of the richest 1 percent continues to grow, in part due to Schedule E income being disproportionately earned by those at the top. To help reverse growing income inequality, Oregon should eliminate tax breaks that certain types of Schedule E income enjoy.

[1] Daniel Hauser and Juan Carlos Ordóñez, Oregon’s Ultra-Rich Continue to Pull Away, Oregon Center for Public Policy, March 6, 2019.

[2] OCPP analysis of Oregon Department of Revenue data. Data in this section includes only full-year returns because of limitations in data availability.

[3] Daniel Hauser, SB 211: End Pass-Through Tax Break, Oregon Center for Public Policy, February 12, 2019.