The federal Affordable Care Act, which marks its second anniversary this month, has set in motion changes that will save money for Oregon small businesses. Businesses large and small have endured rapidly rising costs of providing health coverage to their workers. Fortunately, one of the principal goals of the Affordable Care Act is to rein in costs for small businesses that provide health coverage to their employees.

Because small businesses employ a substantial share of Oregon’s workforce, the state as a whole stands to gain from the Affordable Care Act’s provisions benefiting small businesses.

Download a copy of this issue brief:

How the Affordable Care Act Lowers Costs for Small Businesses (PDF)

Related materials:

Read the commentary An Anniversary Present for Oregon Small Businesses, March 2012

Small Businesses’ Health Coverage Woes Are a Problem for Oregon

Rising health care costs make it difficult for many Oregon small businesses to provide health insurance coverage to their employees. And because small businesses — businesses with fewer than 50 employees — employ one out of three Oregon workers, small businesses’ health coverage woes are a problem for Oregon.[1]

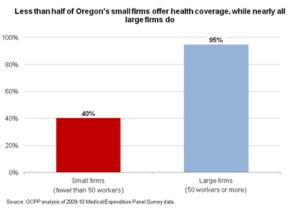

Compared to large firms, small businesses are much less likely to provide health coverage to their workers. In 2009-10, an estimated 40 percent of Oregon firms with less than 50 employees offered health insurance. By contrast, an estimated 95 percent of firms with 50 or more workers offered coverage.[2]

While the share of all private employers offering coverage has been eroding, the decline has been more pronounced among small businesses. In 1999-2000, an estimated 56 percent of Oregon employers offered health coverage. By 2009-10, an estimated 52 percent offered coverage, a 7 percent decline. Over the same period of time, the estimated rate of health coverage among small businesses dropped from 45 percent to 40 percent, an 11 percent decline.[3]

Cost Is the Main Problem Faced by Businesses

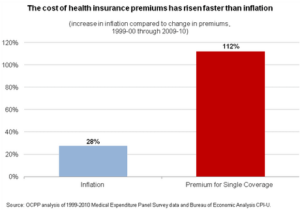

The cost of providing employee health insurance has far outpaced inflation. From 1999-2000 through 2009-10, the rate of inflation rose 28 percent, while the price of insuring one worker rose 112 percent.[4] Taking inflation into account, the cost of insuring one worker increased from an annual average of $2,993 to $4,971. That means the real cost of single coverage increased by 66 percent.[5]

The cost of providing family coverage has also increased sharply, rising 67 percent over the same time period.[6] By 2009-10, it cost on average nearly $13,000 annually to cover an employee and his or her family.[7]

Many businesses share these expenses with their workers. In 2009-10, Oregon employers paid 86 percent of premium costs, with workers picking up the remaining 14 percent.[8] As premiums have skyrocketed over the past decade, both employers and workers have shouldered greater costs.[9]

How the Affordable Care Act Helps Lower Costs for Small Businesses

The Affordable Care Act aims to make health care more accessible and affordable for small businesses. It does so through several mechanisms, some that have taken effect already, and some that will take effect in 2014. Specifically:

Tax credits. The Affordable Care Act lowers costs by providing tax credits to the smallest businesses that insure their workers, a benefit already in effect. The credit targets firms with no more than 25 workers. Currently, these small employers can receive a credit for up to 35 percent of their premium contribution, depending on the firm size and average wages. Once Oregon’s health insurance exchange (discussed below) begins operating, these employers will be eligible for credits worth up to 50 percent of their premium contribution.[10]

Health insurance exchanges. The Affordable Care Act outlines the creation of state-based health insurance exchanges — online marketplaces where small businesses and individuals will be able to purchase affordable, quality health care coverage.[11] Oregon already was developing a health insurance exchange at the time of the enactment of the Affordable Care Act, and the law has boosted Oregon’s effort by providing start-up funding and instituting consumer-friendly health plan requirements.[12]

Set to launch in 2014, Oregon’s health exchange should help small businesses obtain better prices. It will do so by enabling small businesses and individuals to band together to use their collective market share in purchasing coverage, promoting competition among plans. The exchange will also make it easier for small businesses and consumers to compare insurance plans on the basis of price.[13]

New protections. In 2014, the Affordable Care Act will put into effect several new insurance market protections for small businesses and consumers. The Act will bar insurance companies from raising prices on a small business when a worker gets sick.[14] Additionally, customers will receive rebates from insurance companies if companies spend less than 80 percent of the premiums they collect on actual health services and improving care quality.[15] In this way, the Affordable Care Act aims to prevent insurers from excessively profiting from businesses that provide coverage to their workers.

The changes brought about by the Affordable Care Act, including its boost for Oregon’s health insurance exchange, should yield real cost savings for small businesses. The Urban Institute estimates that costs for firms with 100 employees or less will decline by 8.6 percent as a result of the law. They further estimate that the savings will be concentrated among firms with fewer than 50 employees, for whom care costs should decline by as much as 12 percent.[16]

Conclusion

The changes already put in place by the Affordable Care Act, as well as those on the way, should help rein in the costs faced by small businesses that provide health coverage to their employees and make it easier for more small businesses to insure their workers. Given that small businesses employ a substantial share of Oregon’s workforce, these provisions of the Affordable Care Act benefit the state as a whole.

[1] In 2009-10, businesses of fewer than 50 employees comprised 32 percent of Oregon’s workforce. OCPP analysis of Medical Expenditure Panel Survey data. There is no universally accepted definition of “small business.” Unless otherwise noted, this report defines “small businesses” as firms with fewer than 50 employees. Because of the sample size, the two years of data are combined to produce a reliable estimate of change over time.

[2] OCPP analysis of 2009 and 2010 Medical Expenditure Panel Survey data.

[3] OCPP analysis of 1999, 2000, 2009 and 2010 Medical Expenditure Panel Survey data.

[4] In 1999-2000, the estimated non-inflation-adjusted price of the average annual single premium was $2,327. In 2009-2010, the average price of the same premium was $4,933. OCPP analysis of Medical Expenditure Panel Survey and Bureau of Economic Analysis CPI-U data.

[5] The premium price figures are inflation-adjusted to 2010 dollars. The cost of single coverage increased by 66.1 percent between 1999-2000 and 2009-2010. OCPP analysis of Medical Expenditure Panel Survey and Bureau of Economic Analysis CPI-U data.

[6] The increase in family coverage takes into account the effect of inflation.

[7] In 2009-10, the average annual premium for family coverage in Oregon was $12,993. OCPP analysis of Medical Expenditure Panel Survey data.

[8] OCPP analysis of 2009 and 2010 Medical Expenditure Panel Survey data.

[9] Between 1999-2010, the average employer share of single-coverage premiums ranged from 88.1 percent (2000-01) to 86.1 percent (2009-10). Source: OCPP analysis of Medical Expenditure Panel Survey data.

[10] Affordable Care Act, Section 1421.

[11] Affordable Care Act, Section 1311-1334.

[12] To make it easier for consumers to accurately compare plans, the Affordable Act requires that plans, whether sold through an exchange or elsewhere, conform to one of four standardized tiers of coverage. Affordable Care Act, Section 1302(d).The requirement is expected to increase the adequacy of coverage offerings. McMorrow, Stacy, Linda Blumberg, Matthew Buettgens, The Effects of Health Reform on Small Businesses and Their Workers, Urban Institute, June 2011.

[13] Ibid.

[14] Affordable Care Act, Section 1201.

[15] Affordable Care Act, Section 1001/2718 Public Health Services Act (PHSA).

[16] McMorrow, Stacey, Linda J. Blumberg, Matthew Buettgens, The Effects of Health Reform on Small Businesses and Their Workers, Urban Institute, June 2011.

Posted in Health Care.

More about: affordable care act, health care costs, health insurance, health insurance exchange, health reform, small business