Corporations today pay far less in Oregon taxes than they used to — an outcome that did not arrive by accident. Rather, it is largely the result of powerful special interests having manipulated the system to their advantage.

Over the decades, corporate tax contributions in Oregon have shrunk dramatically with respect to both income and property tax collections. This happened as corporations have lobbied for and won many tax loopholes and subsidies, aggressively pursued tax sheltering strategies, and taken advantage of corporate forms largely exempt from corporate income taxes. While the gaming of the system is most evident in the income tax arena, it is also present in the property tax system.

We all want to see thriving communities in Oregon, yet the decline of corporate taxes makes that difficult to achieve. Our schools, public colleges and universities, and public health system serve as foundations for vibrant communities and a strong state economy. These public investments benefit everyone, including corporations. These investments must be paid for, and taxes are how we pay for them. Resources become scarce when corporations game the tax system.

The way forward is clear. Corporations doing business in Oregon must contribute more toward the common good. Lawmakers should close loopholes and end wasteful subsidies as well as enact strong corporate disclosure laws to shed light on corporate tax gaming.

Corporate income taxes have declined dramatically over the decades

Where does the Oregon legislature find the money to pay for schools, public safety, and health and human services? These vital services make up more than 90 percent of the state budget, formally called the Oregon General Fund and Lottery Funds budget.[1] The money for the state budget comes mostly from income taxes. In fact, more than nine out of every 10 state budget dollars comes from the income tax, which depends on two sources: the personal income tax and the corporate income tax.[2]

Over the decades, the Oregon corporate income tax has declined dramatically as a source of revenue. This is evident from several perspectives. First, as a share of the state’s economy, corporate tax contributions have shrunk by more than half since the late 1970s. Second, as a share of all income taxes collected in Oregon, corporate income taxes have also contracted. Third, corporate income taxes have eroded to such an extent that the Oregon Lottery now brings in more revenue than the corporate income tax. And fourth, in recent years many profitable corporations have paid nothing or next-to-nothing in income taxes.

Sadly, absent a significant change in policy, the corporate income tax is projected to continue shriveling in the decades to come.

The corporate income tax has shrunk as a share of the Oregon economy

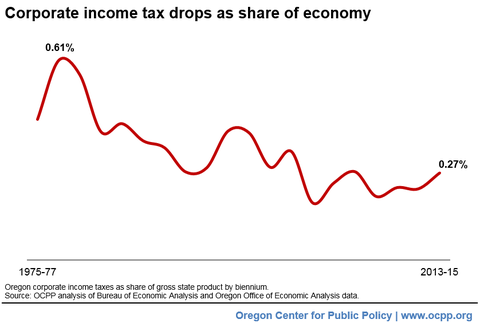

One way to put in perspective the decline of the corporate income tax is to consider how much revenue it generates relative to the size of the Oregon economy. By that measure, the corporate income tax has dropped by more than half.

In the late 1970s, corporate income taxes were 0.61 percent of Oregon’s Gross State Product (GSP), a measure of the Oregon economy.[3]

Over the next several decades, corporate income tax contributions as a share of the economy declined by more than 56 percent. By the 2013-15 budget period, corporate income taxes were just 0.27 percent of Oregon GSP.

This decline occurred even as corporate profits nationally exploded upward. Today, corporate profits as a share of the national economy stand near their all-time high.[4]

The corporate income tax has also dwindled as a share of all income taxes

Another way to assess the decline of the corporate income tax is to consider how much it generates as a share of all income taxes collected in Oregon. By this measure, corporate income taxes have also fallen sharply.

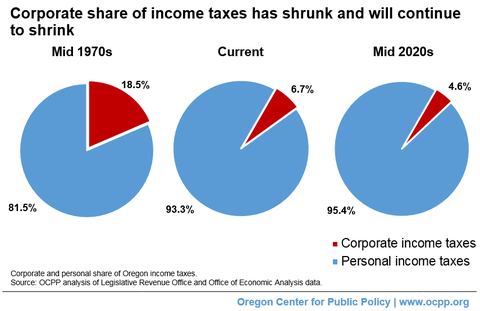

In the 1973-75 budget period, corporations contributed 18.5 percent of all income taxes paid in Oregon, with the rest paid by individuals and families through the personal income tax.[5] Today, in the current (2015-17) budget period, the corporate share of income taxes paid in Oregon is expected to shrink to just 6.7 percent. That is a decline of nearly two-thirds (64 percent).

This picture is expected to worsen in the coming years. According to projections by state economists, revenue from corporate income taxes will remain at its current $1.13 billion per biennium through the 2023-25 budget period.[6] Meanwhile, personal income tax collections are expected to climb 49 percent to $23.4 billion in 2023-25. If those projections come to pass, a decade from now corporations will be contributing just 4.6 percent of all income taxes collected in Oregon.

Thus, absent any significant change in policy, Oregon families and individuals who pay the personal income tax will carry an even bigger share of the responsibility for funding the public services that benefit everyone, including corporations.

The Oregon Lottery now brings in more than the corporate income tax

The decline of the corporate income tax has been so significant that it now brings in less revenue than the Oregon Lottery. In the current budget period, the corporate income tax is expected to bring in $1.13 billion.[7] The Oregon Lottery, in turn, is projected to generate $1.22 billion for the state budget.

The fact that the Oregon Lottery brings in more revenue than the corporate income tax is a true badge of shame. Research shows that state lotteries generate most of their revenue from people struggling economically or with a gambling addiction.[8]So, as corporations have shed their income tax responsibilities over the years, some of the load has fallen on the shoulders of those least able to carry it.

Many corporations have paid nothing or next-to-nothing

Corporations’ success at gaming the system is evident from the fact that, in recent years, some highly profitable corporations have paid nothing — zero — in income taxes, despite Oregon having a minimum income tax for corporations.[9] In 2013, 55 corporations with Oregon sales over $100 million used tax credits to pay less than the minimum tax.[10] And 71 corporations that paid nothing in income taxes in 2013 had Oregon profits of at least half-a-million dollars.[11]

While lawmakers put a stop to this end-run on the minimum tax in 2015, the ban is only temporary.[12] In 2021, corporations will once again have a green light to get around the Oregon corporate minimum tax.

Beyond the hundreds of corporations that have skirted the minimum tax in recent years, many more pay just the minimum, a relatively modest amount. In fact, more than two-thirds of the 29,475 corporations that paid Oregon income taxes paid just the minimum in 2013.[13] That list included 398 corporations with Oregon sales of at least $25 million. Seventy-eight of those paying just the minimum had Oregon sales in excess of $100 million.

The phenomenon of corporations paying nothing or next-to-nothing is not unique to Oregon. When looking at the sum of all state income taxes across the country, 68 Fortune 500 companies paid no state income taxes in at least one year from 2008 to 2010, despite collectively reporting nearly $117 billion in pre-tax profits to their shareholders during that period.[14] Some companies managed to pay no net state income taxes over that full three-year period. That list included Intel, one of Oregon’s largest private sector employers.

Gaming of the system explains much of the corporate income tax decline

The decline of Oregon corporate income taxes did not occur by accident; it happened as a result of corporations gaming the system. The principal ways they have done so are by obtaining numerous tax subsidies and loopholes at both the state and federal level, by pursuing aggressive tax sheltering strategies, and by taking advantage of new corporate forms largely exempt from corporate income taxes.

Corporations have lobbied for and won many tax subsidies and loopholes

Over the past few decades, corporations have lobbied for and won many tax subsidies and loopholes, thereby reducing the amount of taxes they would otherwise pay.

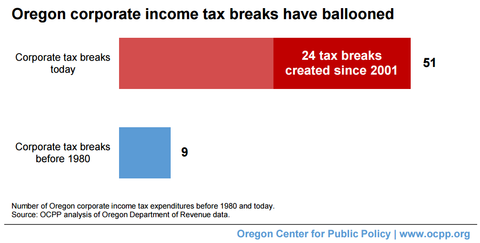

Many of the tax breaks that have eroded Oregon’s corporate income tax base have originated at the federal level.[15] Oregon, like many other states, uses the federal definition of “taxable income” as the starting point for calculating state taxes. As a result, every new corporate tax break affecting the definition of taxable income that Congress puts on the books automatically becomes part of Oregon’s tax system, unless the Oregon legislature affirmatively “decouples” from that provision. Currently, there are 51 corporate income tax breaks that Oregon recognizes because it follows the federal rules.[16]

The Oregon legislature itself has not been shy about granting corporate tax subsidies and loopholes. Right now, corporations enjoy 51 income tax expenditures created by the Oregon legislature.[17] That is in addition to the corporate income tax breaks that exist as a result of changes to the federal tax rules. Only nine of these state-created tax breaks existed before 1980. Nearly half (24) have been created since 2001.

How much are all these corporate income tax breaks costing Oregon? It is safe to say that the figure is in the hundreds of millions of dollars. Adding up the revenue impacts of all the significant corporate income tax breaks listed on the 2015-2017 Oregon Tax Expenditure Report results in a figure of $827 million in foregone revenue in the current budget period.[18] The report, however, cautions about the accuracy of simply adding up the cost of tax expenditures. Still, as the Oregon Department of Revenue explains, the figure offers a “rough order of magnitude” of the total cost of corporate income tax expenditures.

It is important to note that the figures above do not take into account one of the costliest corporate income tax subsidies: single sales factor apportionment. This tax break concerns the formula for calculating how much of the U.S. profits of a multistate corporation Oregon can tax. Before 1991, the formula took into account three factors: a corporation’s in-state sales, its in-state payroll, and its in-state property. Multi-state corporations, however, persuaded the Oregon legislature to phase out the latter two factors. By 2008, the only factor that remained was the amount of sales within Oregon. That change dramatically shrunk the Oregon tax bill for corporations with a big payroll and property footprint in the state that mainly sell outside Oregon, corporations such as Nike and Intel. The 2013-2015 Oregon Tax Expenditure Report estimated the cost of the change to the “single sales factor” formula to be about $165 million for that budget period.[19]

Starting with the 2015-17 Tax Expenditure Report, the Oregon Department of Revenue stopped counting single sales factor as a tax expenditure. Its hefty cost, however, has not disappeared.

Tektronix: Tax subsidies are giveaways

A revealing moment occurred at an April 2015 hearing of the Oregon House Committee on Revenue discussing whether to expand and make refundable Oregon’s Research and Development Tax Credit. In response to a question from a lawmaker, the tax director of Tektronix stated, “[W]ould Tektronix be doing anything different in its business if did not have a credit on its books? I would say no. I’ll be on record saying that.”[20]

Such candor is rarely heard from corporations, but it nicely sums up what the research has found with regard to tax subsidies. State tax subsidies do little to affect business decisions. In fact, because taxes make up only a small share of the cost of doing business, tax giveaways “are rarely the deciding factor in whether a business chooses to hire or invest within a state’s borders.”[21] A review of existing literature concluded that, at best, subsidies “work 10 percent of the time, and are simply a waste of money the other 90 percent.”[22]

Corporations have pursued aggressive tax sheltering strategies

Corporations have also reduced their Oregon corporate income taxes by aggressively utilizing tax shelters.

Tax sheltering refers to legal and illegal strategies pursued for the purpose of reducing or deferring income tax payments.[23] Typically, a corporation shifts profits from the place where they were earned to a location that offers a tax advantage. While the use of offshore tax shelters has received considerable attention in recent years, certain U.S. states (Nevada, Wyoming and Delaware) are also well-known locations for tax shelters.[24] Because the various strategies involve transactions within related companies, tax sheltering is a game usually played by larger corporations.[25]

While it’s difficult to put a precise figure on how much revenue Oregon loses as a result of corporate tax sheltering, the evidence indicates that it is a large figure. A recent study concluded that the revenue loss to the U.S. government due to corporate use of offshore tax havens “likely exceeds $100 billion per year at present.”[26] This huge amount has implications for Oregon. As the Oregon Department of Revenue has pointed out, “As a result of Oregon’s statutory connection to the federal taxable income amount, income shifted offshore via international tax shelters reduces federal and Oregon corporation income tax liabilities.”[27] One study estimated that offshore tax sheltering costs Oregon about $283 million per year.[28]That figure does not include what Oregon loses due to domestic tax sheltering — the shifting of profits to other states within the U.S.[29]

Rise of pass-through companies accounts for a portion of the decline

Over the last three decades, more businesses have opted to incorporate in ways that that are not subject to the corporate income tax. These forms of incorporation include S-corporations, partnerships, and sole proprietorships. Such companies “pass through” their profits to their owners and shareholders to be taxed as personal income. The rise of pass-through entities explains a portion of the decline of corporate taxes, though how much is unclear. Furthermore, pass-through entities create additional opportunities to game the system.

The impact of pass-through entities does not appear significant when viewing the share of business income being declared on Oregon personal income tax returns. Business income made up 10.5 percent of all Oregon income in 2014.[30] That figure was just 3.2 percent higher than the business share of all income in 1993 (10.2 percent), when Oregon began allowing firms to incorporate as “limited liability companies” (LLCs). Corporate income taxes as a share of the Oregon economy declined by nearly a third over that same period.[31]

National researchers, however, have found a significant increase in the business income going to pass-through entities. In 1980, nearly 80 percent of net business income nationally was earned by C-corporations, those corporations subject to Oregon’s corporate income tax, according to a recent study by the National Bureau of Economic Research (NBER).[32] By 2011, C-corporations earned less than half of net business income (46 percent).

This shift toward pass-through entities itself appears to create new opportunities for gaming the tax system. The NBER study found that the largest and fastest-growing category of pass-through entities — partnerships — is also the most opaque. The researchers found that about 30 percent of partnership income flows to partners whose status (individual or foreign corporation, for example) is unclear, or to partners who are yet another partnership, which in turn could be owned by another partnership. “A long-standing rationale for the entity-level corporate income tax is that it can serve as a backstop to the personal income tax system,” the study concludes. “Our inability to unambiguously trace 30 percent of partnership income to either the ultimate owner or the originating partnership underscores the concern that the current U.S. tax code encourages firms to organize opaquely in partnership form in order to minimize tax burdens.”[33]

Besides opening the door to further tax gaming, the rise of pass-through businesses has fueled the growth of income inequality nationally, according to NBER. “As is well known,” the study says, “the [top 1 percent’s] income share doubled (from 10.0 percent to 20.1 percent) between 1980 and 2013. Less well known is that 41 percent of that increase came in the form of higher pass-through business income.”[34]

Corporate property taxes have also declined significantly

Corporations also contribute less in the form of property taxes than they used to. Property taxes are the second largest source of revenue for Oregon public schools, trailing only income taxes.[35] They are also the main way that communities fund services that foster quality of life: libraries, parks and emergency response services, for example. While the decline in corporate property taxes is partly due to tax policy changes in Oregon, it is also the result of corporate tax gaming.

It used to be that, as a group, businesses in Oregon paid more in property taxes than families and individuals. That is no longer true.

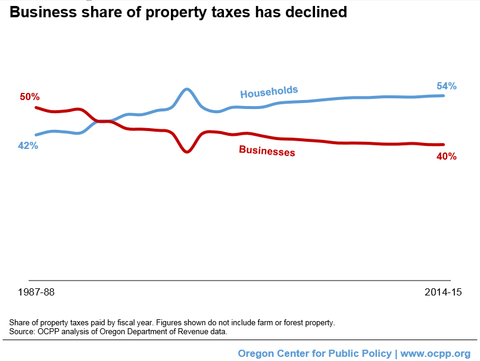

In the 1987-88 fiscal year, businesses contributed about half of all property taxes levied in Oregon and households contributed about 42 percent.[36] Farm and forest property, not included in either the business or household share, made up the remainder.[37]

By the 2014-15 fiscal year, the business share of property taxes had declined to about 40 percent. Meanwhile, the contributions from households increased to 54 percent.

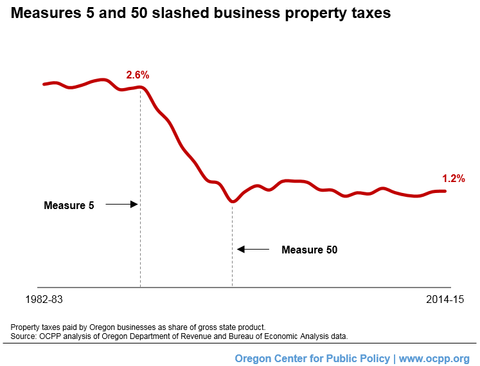

Businesses – including corporations – won big with Measures 5 and 50

What caused this shift in property taxes away from businesses and onto households? Much of it is due to the fact that businesses benefited greatly from seismic changes to Oregon’s property tax system in the 1990s.

Those changes came as a result of two ballot measures enacted by voters: Measures 5 and 50. Approved by voters in 1990, Measure 5 sharply reduced property tax rates.[38] But despite this measure, property taxes continued to rise for families as result of a boom in home values during the early and mid-1990s. In response, voters came back with another ballot measure that would eventually become Measure 50.[39]Measure 50 changed Oregon’s property tax assessments from being based on the market value of a property to an assessed value (determined by government property assessors). Measure 50 also set the maximum assessed value of property for the 1997-98 fiscal year at 90 percent of the real market value in 1995-96 and capped the growth in maximum assessed value to three percent per year.

The net effect of these two measures was to shrink the business share of property taxes paid in Oregon. Measure 5 slashed property taxes, including property taxes paid by corporations and other businesses. Measure 50 then locked in property taxes at a time when commercial property was inexpensive, relative to residential property.[40]

The impact of these measures is clear when looking at property taxes paid by businesses as a share of the state economy.

Throughout the 1980s, property taxes paid by businesses made up about 2.6 percent of the Oregon economy.[41] But following the enactment of Measure 5 in 1990, business property taxes began to fall sharply. The decline continued until the enactment of Measure 50 in 1997.

Since then, property taxes paid by corporations and other businesses as a share of the Oregon economy have been locked in at a lowered rate. During 2014-15 fiscal year, the year with the most recent data, property taxes paid by businesses made up just 1.2 percent of the state economy.

Corporate tax gaming is also to blame

While Measures 5 and 50 are a big part of the story for why businesses today pay far less in property taxes than they used to, corporate tax gaming is also to blame. Over the years, corporations have lobbied for and won substantial property tax subsidies and loopholes. One example is Oregon’s Strategic Investment Program (SIP), a partial property tax exemption whose cost has ballooned from $164 million in 2003-05 to $521 million in the current budget period.[42]

There is little evidence that corporate property tax breaks have a beneficial economic impact. These tax breaks are often justified on the grounds that they help local governments attract and retain business investments. Yet research indicates that these incentives have had mixed results at best, and in general have little effect on where businesses chose to locate and in generating economic activity.[43]

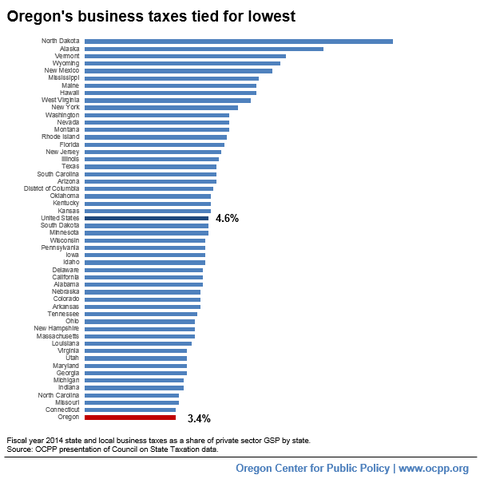

Oregon has nation’s lowest business taxes

After decades of declining corporate taxes, Oregon finds itself at the bottom when it comes to overall business taxes. Despite using different methodologies, two recent studies reached the same conclusion: Oregon ranks last among all states in terms of business taxes.

In a study funded by many of the nation’s largest corporations, Oregon tied Connecticut in having the lowest “total effective business tax rate” in the country.[44]The Council On State Taxation (COST) — a lobbying group representing about 600 corporations, including Nike and Intel — funds a study conducted by the accounting firm Ernst & Young.

The most recent version of the study found that the total state and local taxes paid by Oregon businesses amounted to 3.4 percent of Oregon’s private sector economy in fiscal year 2014, the smallest such total effective business tax rate among all states. The national average was 4.6 percent.

The COST study purports to include all taxes businesses pay: corporate income and excise taxes; property, sales and use, and license taxes paid by businesses; personal income taxes on business income passed through to the personal income tax (such as those taxes paid by owners of S-corporations, partnerships, sole proprietorships, and limited liability companies); unemployment insurance taxes; and other business taxes.

Oregon also ranked lowest in terms of total state and local business taxes in a recent study by the Anderson Economic Group (AEG), which looked at data from fiscal year 2014.[45] Instead of estimating taxes collected as a share of the state economy, as done by COST, AEG examined taxes paid by businesses as a share of “pre-tax operating margin,” one measure of profits. The AEG study considered taxes paid by businesses, such as property, license, personal income on pass through entities, corporate income, unemployment compensation, severance, general sales and gross receipts, and other selective sales taxes.

Using different methodologies, both studies arrived at the same conclusion: Oregon has the nation’s lowest business taxes.

The way forward: raise corporate taxes, close loopholes and enact disclosure

Require corporations to contribute more

Corporations must contribute more to support the schools and other critical public services Oregon communities need to thrive. Oregonians will have an opportunity to ensure that they do, thanks to a measure slated for the November 2016 ballot. This measure would modify Oregon’s corporate minimum tax by establishing a 2.5 percent tax on the Oregon sales of C-corporations over $25 million. According to Oregon’s Legislative Revenue Office, the measure would raise $6 billion each budget period, mainly from large, multi-state corporations. This revenue would enable Oregon to make much-needed, economy-boosting investments in schools, healthcare, and senior services.[46]

Close corporate tax loopholes

Lawmakers can ensure corporations contribute more by closing loopholes and subsidies that drain corporate tax revenue. Until recently, ending any tax expenditure, including any corporate tax loophole or subsidy, required a three-fifths supermajority of the Oregon legislature — or so the legislature thought. But last year, the Oregon Supreme Court ruled that ending a tax expenditure is not a bill for raising revenue. Thus, such a bill is not subject to the supermajority requirement.[47]This means that the hurdle for closing tax loopholes is lower than lawmakers had assumed: a simple majority will suffice. Lawmakers should close tax loopholes and subsidies that do little to boost the Oregon economy and undermine the ability of Oregon communities to thrive.

Enact corporate tax disclosure

To truly reform Oregon’s corporate tax system, it is necessary to make it more transparent. Oregon lawmakers should enact corporate tax disclosure to enable Oregonians to see which corporations are taking advantage of which tax loopholes, and which are paying their fair share in taxes. With that information in hand, Oregonians could determine whether tax breaks and incentives serve a useful purpose and go to the right entities. Corporate tax disclosure would also improve Oregon’s business climate by showing that companies can operate here, pay taxes, and make a profit. Moreover, disclosure would allow Oregonians to acknowledge the corporate actors that do their part to support thriving Oregon communities.[48]

Conclusion

Over the past few decades, Oregon has witnessed a dramatic decline in the taxes — both income and property taxes — contributed by corporations. This decline is largely due to corporations having gamed the tax system to their advantage. As a result, corporations have shed much of their responsibilities for paying for the schools that educate their future employees, the public safety system that protects their property, and the health system that keeps their workers healthy.

This corporate divestment from the public structures that businesses rely on to succeed has meant that working Oregonians, many of whom are already struggling to make ends meet, must shoulder an ever-increasing share of the load. This trend cannot continue if Oregon communities are to thrive.

Ensuring that all Oregonians have a chance to succeed means making stronger investments in the public structures that afford them economic opportunity. Oregon can pay for those investments by requiring corporations to contribute more, closing wasteful tax loopholes and subsidies, and enacting strong corporate tax disclosure laws to give lawmakers the tools needed to end corporate tax gaming.

[1] The 2015-17 General Fund budget appropriated $9.3 billion to education, $4.8 billion to human services and $2.3 billion to public safety, which together made up more than 90 percent of the total $18.0 billion budget. For more see 2016 Oregon Public Finance: Basic Facts, Oregon Legislative Revenue Office, p. B4, available at https://www.oregonlegislature.gov/lro/Documents/Basic%20Facts%202016.pdf.

[2] Of the $18.51 billion in 2015-17 General Fund revenues, the personal income tax contributes $15.71 billion while the corporate income tax contributes $1.13 billion. Together they make up about 91 percent of available revenue for the General Fund. For more see 2016 Oregon Public Finance: Basic Facts, Oregon Legislative Revenue Office, p. B4, available at https://www.oregonlegislature.gov/lro/Documents/Basic%20Facts%202016.pdf.

[3] OCPP analysis of Bureau of Economic Analysis (BEA) and Oregon Office of Economic Analysis (OEA) data. Gross state product (sometimes also referred to as gross domestic product by state) is the value of all goods and services produced within a state as measured by the BEA.

[4] Nationally, corporate after-tax profits were about 9.0 percent of gross domestic product in the fourth quarter of 2015. The historical high of 10.8 percent was set in the first quarter of 2012. OCPP analysis of Bureau of Economic Analysis data.

[5] OCPP analysis of June 2016 Oregon Revenue Forecast and Legislative Revenue Office data.

[6] OCPP analysis of June 2016 Oregon Revenue Forecast and Legislative Revenue Office data.

[7] OCPP analysis of OEA data.

[8] See Garrick Blalock, et. al., Hitting the Jackpot or Hitting the Skids: Entertainment, Poverty, and the Demand for State Lotteries, Cornell University, Department of Applied Economics and Management, December 14, 2004 (finding “a strong and positive relationship” between lottery sales and poverty rates); Kent Grote and Victor A. Matheson, The Economics of Lotteries: A Survey of the Literature, College of Holy Cross, August 2011 (“empirical research uniformly finds . . . that a relatively greater percentage of income is spent on lottery products at lower income levels”); Harry Esteve, “Oregon Lottery: Agency pushes slot machines as problem gamblers pay the price,” The Oregonian, November 25, 2013; Denis C. Theriault, “Video lottery machines easier to find in poor neighborhoods, analysis finds,” The Oregonian, June 3, 2015.

[9] Oregon Center for Public Policy, Hundreds of Corporations Escape the Minimum Tax, March 2015, available at http://www.www.ocpp.org/2015/03/30/fs20150330-corporations-escape-minimum-tax/.

[10] Oregon Corporate Excise and Income Tax: 2015 Edition, Oregon Department of Revenue, 2015, p. 34, available at http://www.oregon.gov/DOR/programs/gov-research/Documents/corporate-excise-income_102-405_2015.pdf.

[11] OCPP analysis of Oregon Department of Revenue data emailed from Mary Fitzpatrick, Oregon Department of Revenue, to Tyler Mac Innis, Oregon Center for Public Policy, March 2, 2016.

[12] The so-called “Con-Way Fix,” referring to the case where the Oregon Supreme Court ruled that the trucking company Con-Way could use tax credits against its minimum tax liability, was included in a 2015 omnibus tax expenditure bill (H.B. 2171). This fix temporarily closed the loophole allowing C-corporations to use tax credits to pay less than the minimum tax. The closure of this loophole is set to sunset in 2021.

[13] Oregon Department of Revenue, Oregon Corporate Excise and Income Tax: 2015 Edition.

[14] Institute on Taxation and Economic Policy and Citizens for Tax Justice, Corporate Tax Dodging In the Fifty States, 2008-2010, December 2011, available at http://www.itep.org/pdf/CorporateTaxDodgers50StatesReport.pdf.

[15] One such tax break is the “stock option loophole,” which allows companies to deduct an executive’s stock option compensation. Though these stock options do not present a real cost to corporations, a recent analysis showed that some, “315 corporations reduced their federal and state corporate income taxes by a combined total of $64.6 billion over the last five years,” using this loophole. For more, see Citizens for Tax Justice, Fortune 500 Corporations Used Stock Option Loophole to Avoid $64.6 Billion in Taxes Over the Past Five Years, June 2016, available at http://ctj.org/pdf/excessstockoption0416.pdf.

[16] Oregon Department of Administrative Services, 2015-2017 Tax Expenditure Report, State of Oregon.

[17] Ibid.

[18] OCPP analysis of Oregon Department of Revenue data. This figure does not include tax expenditures with biennial costs under $100,000. There are 46 such tax expenditures for corporations. For more, see State of Oregon, 2015-17 Tax Expenditure Report, Appendix E, available at http://www.oregon.gov/DOR/programs/gov-research/Documents/full-tax-expenditure_2015-17.pdf.

[19] Oregon Department of Administrative Services, 2013-15 Tax Expenditure Report, State of Oregon p. 211, available at http://www.oregon.gov/DOR/programs/gov-research/Documents/tax-expenditure-report_2013-15.pdf.

[20] Mark Modjeski, oral testimony given before the Oregon House Committee on Revenue, April 2, 2015, available at http://www.www.ocpp.org/2015/04/13/blog20150413corporation-tektronix-truth-subsidy/.

[21] Carl Davis, Tax Incentives: Costly for States, Drag on the Nation, Institute on Taxation and Economic Policy, August 2013, available at http://www.itep.org/pdf/taxincentiveeffectiveness.pdf.

[22] Alan Peters and Peter Fisher, “The Failures of Economic Development Incentives,” Journal of the American Planning Association, Vol. 70 No. 1, Winter 2014, available at http://www.crcworks.org/cfscced/fisher.pdf.

[23] Oregon Department of Revenue, Out-of-State Tax Shelters Report, January 2014, p. 1, available at https://www.oregon.gov/DOR/about/Documents/bn_tax-shelters_2014.pdf.

[24] In recent years Oregon has taken steps to address offshore tax sheltering, but those efforts are incomplete. Oregon now requires corporations to add to their Oregon tax returns the income and apportionment factors from subsidiaries located in certain territories deemed to be tax havens. There are currently 44 territories that Oregon defines as tax havens. However, the state’s current list of tax havens excludes some of the biggest centers for offshore tax sheltering, such as the Netherlands, Ireland, and Switzerland.

[25] Oregon Department of Revenue, Out-of-State Tax Shelters Report, January 2014, p. i.

[26] Kimberly A. Clausing, Profit Shifting and U.S. Corporate Tax Policy Reform, Washington Center for Equitable Growth, May 10, 2016, available at http://equitablegrowth.org/report/profit-shifting-and-u-s-corporate-tax-policy-reform/.

[27] Oregon Department of Revenue, Out-of-State Tax Shelters Report, January 2014, p. 10.

[28] OSPIRG, The Hidden Cost of Offshore Tax Havens: State Budgets Under Pressure from Tax Loophole Abuse, January 2013.

[29] Ibid. Further, Oregon remains exposed to domestic tax sheltering. States can protect themselves from domestic tax sheltering by enacting “combined reporting.” Combined reporting treats the parent company and most subsidiaries as one corporation for state income tax purposes. While Oregon is often listed among the states that require combined reporting, that is not fully the case, leaving “Oregon more susceptible to these domestic tax shelters than states that impose . . . combined reporting,” according to the Oregon Department of Revenue. See Oregon Department of Revenue, Out-of-State Tax Shelters Report, January 2014, p. 12.

[30] “Business income” includes income from proprietorships, S-corporations, LLCs, partnerships, rental properties, royalties and trusts. OCPP analysis of Oregon Department of Revenue data.

[31] OCPP analysis of BEA and OEA data.

[32] Michael Cooper, et. al, Business in the United States: Who Owns it and How Much Tax Do They Pay?, National Bureau of Economic Research, January 2016, available at http://www.nber.org/papers/w21651.pdf.

[33] Ibid, pp. 23-24.

[34] Ibid, p. 2.

[35] Oregon Legislative Revenue Office, 2016 Oregon Public Finance: Basic Facts, p. G3, available at https://www.oregonlegislature.gov/lro/Documents/Basic%20Facts%202016.pdf.

[36] OCPP analysis of Department of Revenue data. This analysis utilizes a method of dividing business and household property taxes modified from the Governor’s Tax Review Technical Advisory Committee in its Review of Oregon’s Tax System, released in June 1988. This method includes the following classes of property as business property: industrial, commercial (including multi-housing), farm, forest, personal business, utility, recreational, and “other” property. For this analysis, farm and forest property have been removed from both the personal and business share of property (see endnote 33). “Other” property has also been removed. This methodology does not account for business property tax breaks, and therefore, may overstate the share of property taxes paid by businesses.

[37] Farm and forest property can be difficult to categorize as either personal or business property. For example, a farm can be a person’s residence and business. For that reason, we do not include farm or forest property in either the household or business share of all property taxes.

[38] Measure 5 capped property taxes for schools to $5 for every $1,000 in property value (a 0.5 percent rate) and property taxes for government operations to $10 for every $1,000 in property value (a 1 percent rate).

[39] Measure 50 began as Measure 47 on the November 1996 ballot. Voters approved Measure 47, but the Legislative Assembly revised the measure due to drafting errors. Voters passed the revised measure, Measure 50, which the Legislature referred to voters in May 1997.

[40] Oregon Legislative Revenue Office, Oregon’s Property Tax System: Horizontal Inequities under Measure 50, September 2010, p. 2, available at https://www.oregonlegislature.gov/lro/Documents/rr4-10H_InequitiesUnderMeasure50_092210.pdf.

[41] OCPP analysis of Oregon Department of Revenue and Bureau of Economic Analysis data. To estimate property taxes as a share of the economy, we multiply total property taxes paid in Oregon by the respective business property share (see endnote 35) and divide that figure by Oregon’s GSP.

[42] For 2003-05 estimate of the foregone revenues from the Strategic Investment Program, see State of Oregon, 2003-05 Tax Expenditure Report, p. 214, available at http://www.oregon.gov/DOR/programs/gov-research/Documents/FullReport_2003-05.pdf. For 2015-17 estimate see State of Oregon, 2015-17 Tax Expenditure Report, p. 297, available at http://www.oregon.gov/DOR/programs/gov-research/Documents/full-tax-expenditure_2015-17.pdf.

[43] Daphne A. Kenyon, Adam H. Langley and Bethany P. Paquin, Rethinking Property Tax Incentives for Business, Lincoln Institute of Land Policy, 2012.

[44] Council On State Taxation, Total State and Local Business Taxes: State-by-state estimates for fiscal year 2014, October 2015, available at http://www.cost.org/WorkArea/DownloadAsset.aspx?id=91531.

[45] Anderson Economic Group, 2016 State Business Tax Burden Rankings, 7th Edition, May 18, 2016.

[46] The Legislative Revenue Office’s analysis of IP 28 concluded that the measure would raise more than $6 billion per biennium while “modestly affecting” the Oregon economy. The model used in the LRO analysis, the authors note, does not factor in the positive economic effects resulting from investments in education, healthcare, and senior services. For LRO’s analysis of IP 28, see Oregon Legislative Revenue Office, Initiative Petition 28 Description and Analysis, May 2016, p. 17, available at http://www.www.ocpp.org/media/uploads/pdf/2016/05/20160523-LRO-IP28-report.pdf. For a review of fiscal policies that can boost state economies, see Erica Williams, A Fiscal Policy Agenda for Stronger State Economies, Center on Budget and Policy Priorities, April 2016, available at http://www.cbpp.org/research/state-budget-and-tax/a-fiscal-policy-agenda-for-stronger-state-economies and Josh Bivens, Public Investment: The next “new thing” for powering economic growth, Economic Policy Institute, April 2012, available at http://www.epi.org/publication/bp338-public-investments/.

[47] City of Seattle v. Dept. of Rev. 357 Or 718 (2015), available at http://www.www.ocpp.org/media/uploads/pdf/2016/06/20150911-seattle-v-dept-revenue.pdf.

[48] For more on corporate tax disclosure see Michael Mazerov, State Corporate Tax Disclosure: The Next Step in Corporate Tax Reform, Center on Budget and Policy Priorities, February 2007, available at http://www.cbpp.org/research/state-corporate-tax-disclosure-the-next-step-in-corporate-tax-reform.

Read the executive summary of this report

Read the news release: Study: Oregon corporate taxes have fallen dramatically over decades