“Grand Bargain” Tax Package Comes with Shrinking Revenue from Tax Subsidy for the 1 Percent and No Jobs

The revenue package that Governor Kitzhaber has presented to the Oregon legislature to consider in a special session starting September 30 suffers from three major flaws: revenue shrinks after the current budget period, it’s mainly a tax cut for some of Oregon’s wealthiest 1 percent, and it won’t create any jobs, despite what its proponents claim. Removing the subsidy for the wealthy would help ensure that the tax package raises enough revenue in future budget periods to support the new investments, and would be more in line with taxpayers’ ability to pay.

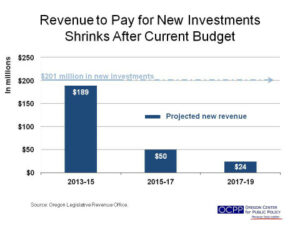

The package’s first flaw is that while the proposal purports to raise $189 million in new revenue to help pay for $201 million in new investments in education, mental health care and services for seniors, the Governor’s plan only fully pays for those investments in the current budget period (2013-15). After that, the revenue raised by the tax plan shrinks to $50 million in 2015-17, and by half again in the 2017-19 budget period to just $25 million. That’s an 87 percent revenue drop. Thus, the plan leaves large funding gaps for those new investments in subsequent budget periods.

Related Materials

See Slideshow: Analysis of Tax Provisions in “Grand Bargain”

Download a copy of this issue brief:

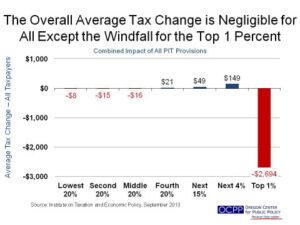

Second, at a time of heightened income inequality, the tax package hands a large tax cut to a portion of Oregon’s wealthiest 1 percent. These wealthiest Oregonians on average would get a tax cut of about $2,700, while the rest of Oregon taxpayers would either see a miniscule tax reduction or a modest tax increase.[1]

And third, a costly provision that would provide a tax subsidy targeted for Oregon’s wealthiest business owners is not tied to any job creation requirement and could reward wealthy business owners who lay off workers.

By eliminating the costly wealthy business-owner tax subsidy, the legislature could ensure that the tax package raises enough revenue to pay for the new investments in subsequent budget cycles and that the package is better aligned with taxpayers’ ability to pay.

Shrinking Revenue Won’t Pay for New Investments

As presently structured, the revenue raised by the tax package shrinks after the current biennium and falls short of what will be required to maintain the proposed investments. The Governor’s plan calls for about $201 million in new investments in education, mental health care, and for services for seniors.[2] In the current budget period, the bulk of the money to pay for those new investments comes from the revenue package. But in subsequent budget periods, the revenue raised from the package falls off sharply.

How rapidly does the revenue decline? The Legislative Revenue Office (LRO) projects that the revenue raised by the package begins at $189 million in 2013-15, then drops to $50 million in 2015-17 and to $24 million in 2017-19, an 87 percent decline.[3]

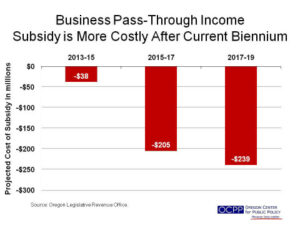

The sharp decline in revenue stems from the ballooning costs of the tax subsidy for wealthy business owners. The plan proposes to offer certain owners of S-corporations and limited liability companies (LLCs) the choice of lower rates on income “passed through” to the owner and taxed as personal income. The income would not be subject to subtractions and deductions. LRO projects that the revenue lost as a result of this tax subsidy jumps from $38 million in 2013-2015, to $205 million in 2015-17, and to $239 million in 2017-19.[4]

In summary, the Governor’s plan falls short of funding its proposed new investments in subsequent budget periods because of the generous tax subsidy for certain wealthy business owners.

It’s Largely a Tax Cut for Some in The Top 1 Percent

As currently structured, the revenue package by-and-large constitutes a tax cut for some of the wealthiest Oregonians.

The package contains several elements that improve Oregon’s personal income tax structure:[5]

- It enacts a modest increase to the Oregon Earned Income Tax Credit, which helps low-income working families make ends meet.

- It caps and reforms the “additional medical deduction.” In its current form, this tax deduction disproportionately benefits well-off seniors, and the loss of tax revenue resulting from it is slated to grow rapidly.

- It eliminates the personal tax exemption credit for high-income earners. Specifically, it changes the current phase-down for wealthy taxpayers by cutting it off lower in the income scale and fully eliminating it for the wealthiest filers.

But these positive changes to Oregon’s personal income tax structure don’t go far enough to offset the damage caused by the provision giving certain owners of S-corporations and LLCs the option of a lower personal income tax rate on passed-through business income.

The provision for certain owners of S-corporations and LLCs alone transforms the revenue package into a proposal that disproportionately benefits Oregon’s wealthiest 1 percent — taxpayers who make over $352,000 a year.[6] When all personal income tax provisions in the package are factored in, Oregonians who make under $55,000 a year get an annual tax reduction of just $16 or less on average. Those making over $55,000 a year see their taxes increase modestly — except for the some of wealthiest 1 percent. Rather than seeing their taxes rise, the wealthiest group of Oregonians gets a tax cut of about $2,700 on average. (Apart from the average impact among the entire top 1 percent, the average tax cut for the members of the top 1 actually receiving a tax cut would be about $6,000).

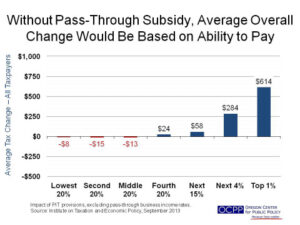

If lawmakers were to exclude the wealthy business income pass-through provision, the revenue-raising package would become much more equitable, in addition to being better able to fund the new investments in future budget periods. For instance, without the wealthy business pass-through provision, the wealthiest 1 percent would experience a $614 tax increase on average instead of a $2,700 tax cut.

Business-Owner Tax Cut Won’t Create Jobs

The tax subsidy for certain business owners contained in the revenue package will not create jobs. Proponents of this provision benefiting certain owners of S-corporations and LLCs tout it as a plan to create jobs, yet the proposal comes with no requirement that the beneficiaries of the tax subsidy actually create any jobs. The package holds no one accountable. Indeed, should the proposal become law, a business owner could lay off employees and still pocket the tax savings.

The proposal, ultimately, hangs on the erroneous premise that reducing taxes for wealthy business owners creates jobs. The research shows that cutting taxes on small business owners is a flawed strategy if the goal is to create jobs.[7] Part of the reason is that customer demand, not tax rates, drives the need for new employees.

That flawed strategy is evident in the Governor’s tax package. Under the tax package’s pass-through provision, those among Oregon’s wealthiest 1 percent who would actually receive a tax subsidy would get about $6,000 in tax savings on average. While $6,000 may pay for a nice family ski vacation, it’s not enough to pay for even a half-time person working a minimum wage job.

Conclusion

While the goal of investing more in education, mental health and services for seniors is laudable, the “Grand Bargain” tax package is the wrong way of trying to achieve that goal.

Lawmakers, however, can correct the flaws in the tax package simply by eliminating the business pass-through income provision. Doing so would enable the tax package to better fund the new investments in subsequent budget cycles, would avoid handing a large tax subsidy to the wealthiest 1 percent and would make the overall tax package more equitable, because the overall impact of the package would be to ask the wealthiest Oregonians to contribute more proportionately.

A revised tax package without the business pass-through income provision would make the special session truly special.

[1] This analysis of the distribution of the personal income tax changes does not include the tax subsidy for interest charge – domestic international sales corporations (IC-DISCs). The overall revenue impacts, however, come from a Legislative Revenue Office analysis that does include the IC-DISC proposed subsidy.

[2] Revenue estimates include all components of the tax plan, including a change in the corporate income tax rate (see note 5 for more detail), elimination of the personal exemption credit for high-income households, restructuring the additional medical deduction, increasing the tobacco tax, introducing the optional rate for certain owners of S-corporations and LLCs, establishing the Oregon IC-DISC (see note 5 for more detail), and increasing the Oregon Earned Income Tax Credit from 6 percent to 8 percent of the federal credit. The Governor’s plan lists the increase in the EITC as an investment. For the purposes of this analysis, OCPP has included this provision in the analysis of the revenue proposal. See Governor Kitzhaber, Legislative leaders come to agreement on additional school funding, PERS reform, assistance for small business and working families, press release, September 18, 2013.

[3] The revenue estimates come from preliminary estimates made by the Legislative Revenue Office and emailed to OCPP on September 24, 2013. The Governor has not shared the actual bill language and reportedly some of the details are not yet final.

[4] Because LRO has acknowledged its lack of confidence in its estimates of the cost of the business pass-through provision, some lawmakers are considering including “sideboards” that contain the cost of the provision.

[5] The revenue package also contains some elements that affect other parts of Oregon’s tax structure, not the personal income tax part. The package institutes a higher tax rate, 7.6 percent, on Oregon corporate profits above $1 million. It raises taxes on tobacco. And it creates an Oregon Interest Charged — Domestic International Sales Corporation (IC-DISC) to permit farmers to pay a lower tax rate on about half of exported sales.

[6]The income levels reflected in the charts in this analysis, based on The Institute on Taxation and Economic Policy’s estimates for all Oregonians in 2013, are the following: The lowest earning 20 percent (the bottom quintile) earn less than $20,000 a year. The average annual income of this group is $12,000. The second lowest 20 percent (the second quintile) earn $20,000 to $34,000 a year. The average annual income of this group is $26,000. The middle 20 percent (the third quintile) earn $34,000 to $55,000 a year. The average annual income of this group is $43,000. The second highest 20 percent (the fourth quintile) earn $55 ,000 to $86,000 a year. The average annual income of this group is $69,000. The next 15 percent earn $86,000 to $166,000 a year. The average annual income of this group is $115,000. The next 4 percent earn $166,000 to $352,000 a year. The average annual income of this group is $224,000. The top 1 percent earn $352,000 or more a year. The average annual income of this group is $807,000.

[6] Mazerov, Michael, Cutting State Personal Income Taxes Won’t Help Small Businesses Create Jobs and May Harm State Economies, Center on Budget and Policy Priorities, February 19, 2013.